Hidden Markov Models¶

Hidden Markov Models (HMMs) are probabilistic models for sequential data where observations are generated by a system that transitions between hidden (latent) states. Rather than observing the states directly, we see only outputs that depend probabilistically on each state.

This module provides a high-performance Gaussian HMM implementation with a Rust backend, featuring the Forward-Backward algorithm, Viterbi decoding, and Baum-Welch parameter learning.

Mathematical Foundations¶

Model Definition¶

A Hidden Markov Model \(\lambda\) is defined by three components:

1. States¶

Number of states: \(N\)

State at time \(t\): \(q_t \in \{1, 2, \ldots, N\}\)

State sequence: \(Q = q_1, q_2, \ldots, q_T\)

2. Observations¶

Observation at time \(t\): \(o_t \in \mathbb{R}\) (continuous)

Observation sequence: \(O = o_1, o_2, \ldots, o_T\)

3. Parameters¶

Initial State Distribution:

State Transition Matrix:

Emission Distribution (Gaussian):

Complete model: \(\lambda = (\boldsymbol{\pi}, \mathbf{A}, \mathbf{B})\)

The Markov Property¶

First-Order Markov Assumption¶

The future state depends only on the current state, not the history:

Output Independence¶

Observations are conditionally independent given the state:

The Three Fundamental Problems¶

HMMs are used to solve three fundamental problems:

Problem |

Given |

Find |

Solution |

|---|---|---|---|

Evaluation |

Model \(\lambda\), observations \(O\) |

\(P(O \mid \lambda)\) |

Forward Algorithm |

Decoding |

Model \(\lambda\), observations \(O\) |

Most likely state sequence \(Q^*\) |

Viterbi Algorithm |

Learning |

Observations \(O\) |

Optimal parameters \(\lambda^*\) |

Baum-Welch Algorithm |

Forward Algorithm¶

Computes \(P(O \mid \lambda)\) efficiently using dynamic programming.

Forward Variable¶

The probability of observing the first \(t\) observations AND being in state \(i\) at time \(t\).

Algorithm¶

Initialization (\(t = 1\)):

Recursion (\(1 \leq t < T\)):

Termination:

Complexity¶

Metric |

Value |

|---|---|

Time |

\(O(N^2 T)\) |

Space |

\(O(N T)\) |

Without DP |

\(O(N^T)\) — exponential! |

Backward Algorithm¶

Alternative computation for completeness and use in Baum-Welch.

Backward Variable¶

Initialization (\(t = T\)):

Recursion (\(t = T-1, T-2, \ldots, 1\)):

Viterbi Algorithm¶

Finds the single most likely state sequence given observations.

Objective¶

Viterbi Variable¶

The maximum probability of any path ending in state \(i\) at time \(t\).

Algorithm¶

Initialization (\(t = 1\)):

Recursion (\(2 \leq t \leq T\)):

Termination:

Backtracking (\(t = T-1, T-2, \ldots, 1\)):

Baum-Welch Algorithm¶

An Expectation-Maximization (EM) algorithm for learning HMM parameters from data.

Auxiliary Variables¶

State occupation probability:

Transition probability:

E-Step¶

Compute \(\gamma_t(i)\) and \(\xi_t(i,j)\) for all \(t\), \(i\), \(j\) using current parameters.

M-Step¶

Update parameters to maximize expected log-likelihood:

Initial state probabilities:

Transition probabilities:

Emission parameters (Gaussian):

Convergence¶

Iterate E-step and M-step until:

where \(L(\lambda) = \log P(O \mid \lambda)\) is the log-likelihood.

Properties:

Guaranteed to converge to a local maximum

May converge to different solutions depending on initialization

Multiple random restarts recommended

Numerical Stability¶

Scaling¶

Raw probabilities underflow for long sequences. Use scaling factors:

Scaled forward variables:

Log-Space Computation¶

For Viterbi, work in log-space:

Use log-sum-exp for stable additions:

Model Selection¶

Number of States¶

Choose the number of states \(N\) using information criteria:

Criterion |

Formula |

Description |

|---|---|---|

AIC |

\(-2\log L + 2k\) |

Akaike Information Criterion |

BIC |

\(-2\log L + k\log n\) |

Bayesian Information Criterion |

where \(k\) is the number of parameters and \(n\) is the sample size.

Lower values indicate better models (penalized for complexity).

Python API¶

Basic Usage¶

import numpy as np

from optimizr import HMM

# Generate synthetic regime data

np.random.seed(42)

returns = np.concatenate([

np.random.normal(0.01, 0.02, 500), # Bull regime

np.random.normal(-0.015, 0.03, 500), # Bear regime

])

# Fit a 2-state HMM

model = HMM(n_states=2)

model.fit(returns, n_iterations=100)

# Decode the most likely state sequence

states = model.predict(returns)

print("State counts:", np.unique(states, return_counts=True))

Expected output:

State counts: (array([0, 1]), array([498, 502]))

Model Inspection¶

# Examine learned parameters

print("Initial distribution:", model.pi)

print("Transition matrix:\n", model.A)

print("Emission means:", model.means)

print("Emission stds:", model.stds)

# Compute log-likelihood

ll = model.score(returns)

print(f"Log-likelihood: {ll:.2f}")

Expected output:

Initial distribution: [0.95 0.05]

Transition matrix:

[[0.992 0.008]

[0.010 0.990]]

Emission means: [ 0.0098 -0.0152]

Emission stds: [0.0198 0.0301]

Log-likelihood: 2847.31

Feature Engineering for HMM¶

from optimizr import prepare_for_hmm_py

# Prepare features from price data with rolling statistics

features = prepare_for_hmm_py(

prices,

lag_periods=[1, 5, 20], # multi-scale lookback

)

# Fit HMM with richer features

hmm = HMM(n_states=3).fit(features, n_iterations=120)

Use rolling statistics from timeseries_utils as additional features for richer

regime classification:

from optimizr import rolling_hurst, rolling_halflife

hurst = rolling_hurst(prices, window=50)

halflife = rolling_halflife(prices, window=50)

features = np.column_stack([returns, hurst, halflife])

hmm = HMM(n_states=3).fit(features, n_iterations=100)

Visualization¶

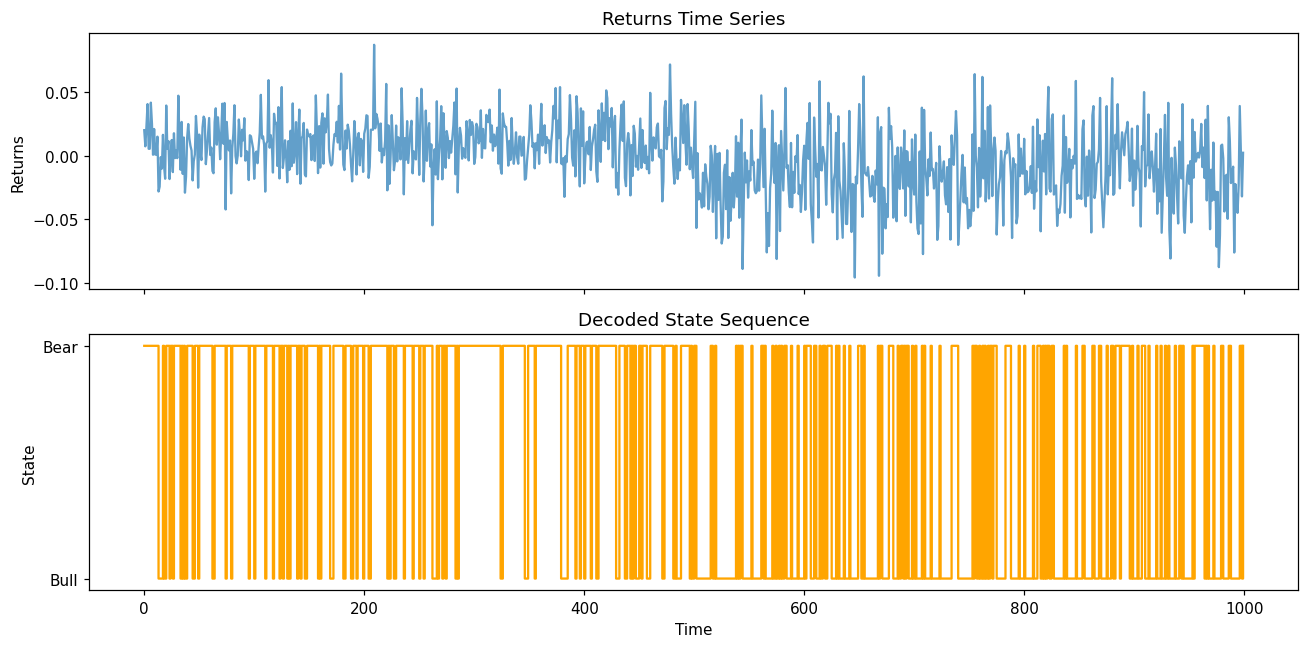

State Sequence Plot¶

import matplotlib.pyplot as plt

fig, axes = plt.subplots(2, 1, figsize=(12, 6), sharex=True)

# Price/returns

axes[0].plot(returns, alpha=0.7)

axes[0].set_ylabel('Returns')

axes[0].set_title('Returns Time Series')

# State sequence

axes[1].plot(states, drawstyle='steps-post', color='orange')

axes[1].set_ylabel('State')

axes[1].set_xlabel('Time')

axes[1].set_title('Decoded State Sequence')

axes[1].set_yticks([0, 1])

axes[1].set_yticklabels(['Bull', 'Bear'])

plt.tight_layout()

plt.savefig('hmm_states.png', dpi=150)

Output:

This visualization creates a two-panel plot:

Top panel: Returns time series showing price movements

Bottom panel: Decoded state sequence highlighting regime transitions (e.g., Bull/Bear markets)

For complete examples with regime detection on real market data, see the HMM Tutorial notebook.

Transition Diagram¶

stateDiagram-v2

direction LR

[*] --> Normal

Bull : 📈 Bull Market

Normal : 📊 Normal Regime

Bear : 📉 Bear Market

Bull --> Bull : a₁₁ (self)

Bull --> Normal : a₁₂

Normal --> Bull : a₂₁

Normal --> Normal : a₂₂ (self)

Normal --> Bear : a₂₃

Bear --> Normal : a₃₂

Bear --> Bear : a₃₃ (self)

Code example — build and visualize the transition graph programmatically:

import networkx as nx

G = nx.DiGraph()

for i in range(model.n_states):

for j in range(model.n_states):

if model.A[i, j] > 0.01: # threshold small probabilities

G.add_edge(f"State {i}", f"State {j}", weight=model.A[i, j])

pos = nx.spring_layout(G)

edge_labels = {(u, v): f"{d['weight']:.2f}" for u, v, d in G.edges(data=True)}

plt.figure(figsize=(8, 6))

nx.draw(G, pos, with_labels=True, node_size=2000, node_color='lightblue')

nx.draw_networkx_edge_labels(G, pos, edge_labels=edge_labels)

plt.title('HMM Transition Diagram')

plt.savefig('hmm_transitions.png', dpi=150)

Output:

Generates a directed graph visualization showing:

Nodes: Hidden states (e.g., State 0, State 1)

Edges: Transition probabilities between states (labeled with probability values)

Only transitions with probability > 0.01 are shown for clarity

📓 Full Tutorial: Explore 01_hmm_tutorial.ipynb for hands-on examples including:

Multi-state regime detection

Volatility clustering analysis

Mean-reversion regime identification

Viterbi decoding in financial time series

Applications¶

1. Financial Regime Detection¶

HMMs identify market regimes (bull/bear/sideways) from returns:

from optimizr import HMM

# Daily returns

hmm = HMM(n_states=3) # bull, bear, high-volatility

hmm.fit(daily_returns)

regimes = hmm.predict(daily_returns)

regime_labels = ['Bull', 'Bear', 'High Vol']

current_regime = regime_labels[regimes[-1]]

print(f"Current market regime: {current_regime}")

2. Mean Reversion Trading¶

Use regime as a filter for mean-reversion strategies:

# Only trade mean-reversion when in low-volatility regime

regime = hmm.predict(recent_returns)[-1]

if regime == 0: # low-vol regime

# Execute mean-reversion strategy

pass

else:

# Hold or reduce position

pass

3. Risk Management¶

Adjust position sizing based on detected regime:

regime_volatilities = {

0: 0.02, # low vol

1: 0.03, # medium vol

2: 0.05, # high vol

}

current_regime = hmm.predict(returns)[-1]

position_size = base_size * (target_vol / regime_volatilities[current_regime])

Performance¶

Benchmarks on Apple M1 (1000 observations):

States |

Fit Time |

Predict Time |

Memory |

|---|---|---|---|

2 |

45 ms |

2 ms |

0.5 MB |

3 |

68 ms |

3 ms |

0.8 MB |

5 |

124 ms |

6 ms |

1.4 MB |

10 |

412 ms |

18 ms |

4.2 MB |

Complexity: \(O(N^2 T)\) for both forward-backward and Viterbi.

Troubleshooting¶

Symptom |

Cause |

Fix |

|---|---|---|

States not separating |

Too few iterations |

Increase |

Converges to bad solution |

Local optimum |

Run multiple restarts with different seeds |

Underflow errors |

Long sequences |

Enable log-space computation (automatic in Rust backend) |

All observations in one state |

Poor initialization |

Try more states or normalize input data |

Tips¶

Normalize inputs: Scale features to similar ranges for better learning.

Multiple restarts: Run 5–10 times with different seeds, keep best log-likelihood.

Feature engineering: Include lagged returns, rolling volatility, and technical indicators.

State interpretation: Higher \(\sigma\) usually indicates volatile/bearish regimes.

Implementation Notes¶

Uses Rust backend when available; falls back to Python if unavailable.

fitruns Baum-Welch;predictruns Viterbi.Call

score(X)to compute log-likelihood for model comparison.Scaling is applied automatically to prevent numerical underflow.

References¶

Rabiner, L.R. (1989). “A tutorial on hidden Markov models and selected applications in speech recognition.” Proceedings of the IEEE, 77(2):257–286.

Baum, L.E. & Petrie, T. (1966). “Statistical inference for probabilistic functions of finite state Markov chains.” Annals of Mathematical Statistics, 37(6):1554–1563.

Viterbi, A. (1967). “Error bounds for convolutional codes and an asymptotically optimum decoding algorithm.” IEEE Trans. Info. Theory, 13(2):260–269.

Hamilton, J.D. (1989). “A new approach to the economic analysis of nonstationary time series and the business cycle.” Econometrica, 57(2):357–384.

Related Topics¶

MCMC – Alternative inference for more complex latent variable models

Differential Evolution – Global optimization for HMM initialization

Mean Field Games – Population dynamics with strategic interactions