MCMC Sampling¶

Markov Chain Monte Carlo (MCMC) methods are a class of algorithms for sampling from probability distributions by constructing a Markov chain whose stationary distribution equals the target distribution. MCMC is fundamental to Bayesian inference, computational statistics, and quantitative finance.

This module provides a high-performance Metropolis-Hastings sampler with Rust acceleration, designed for Bayesian parameter estimation and posterior exploration.

Mathematical Foundations¶

The Monte Carlo Goal¶

Sample from a target distribution \(\pi(\theta)\) where:

Direct sampling is difficult or impossible

We can evaluate \(\pi(\theta)\) up to a normalization constant

Given samples \(\theta^{(1)}, \ldots, \theta^{(N)} \sim \pi(\theta)\), we approximate:

Expectations:

Probabilities:

Quantiles, posterior intervals, and other distributional properties.

Markov Chains¶

A sequence \(\theta^{(0)}, \theta^{(1)}, \theta^{(2)}, \ldots\) is a Markov chain if:

The next state depends only on the current state.

Transition Kernel¶

Stationary Distribution¶

A distribution \(\pi(\theta)\) is stationary if:

If we start with \(\theta^{(0)} \sim \pi\), then \(\theta^{(t)} \sim \pi\) for all \(t\).

Ergodicity¶

A Markov chain is ergodic if:

Irreducible: Can reach any state from any state

Aperiodic: No cyclic behavior

For ergodic chains with stationary distribution \(\pi\):

regardless of initial state \(\theta^{(0)}\).

Detailed Balance¶

A sufficient condition for \(\pi\) to be stationary:

Reversibility: The probability of going \(\theta \to \theta'\) equals that of \(\theta' \to \theta\).

Metropolis-Hastings Algorithm¶

The MH algorithm constructs a Markov chain whose stationary distribution is the target \(\pi(\theta)\).

Algorithm¶

Input: Target distribution \(\pi(\theta)\), proposal distribution \(q(\theta' \mid \theta)\)

Algorithm: Metropolis-Hastings

──────────────────────────────

1. Initialize θ⁽⁰⁾

2. For t = 0, 1, 2, ..., N-1:

a. Propose: Draw θ* ~ q(θ* | θ⁽ᵗ⁾)

b. Compute acceptance probability:

α = min(1, [π(θ*) · q(θ⁽ᵗ⁾|θ*)] / [π(θ⁽ᵗ⁾) · q(θ*|θ⁽ᵗ⁾)])

c. Accept or reject:

u ~ Uniform(0, 1)

if u < α:

θ⁽ᵗ⁺¹⁾ = θ* # accept

else:

θ⁽ᵗ⁺¹⁾ = θ⁽ᵗ⁾ # reject

3. Return samples {θ⁽¹⁾, θ⁽²⁾, ..., θ⁽ᴺ⁾}

Acceptance Probability¶

The ratio \(\pi(\theta^*)/\pi(\theta^{(t)})\) compares likelihoods. The ratio \(q(\theta^{(t)} \mid \theta^*)/q(\theta^* \mid \theta^{(t)})\) corrects for asymmetric proposals.

Why It Works¶

Theorem: The MH algorithm produces a Markov chain with stationary distribution \(\pi(\theta)\).

The acceptance rule ensures detailed balance holds, guaranteeing convergence to \(\pi\).

Special Cases¶

Metropolis Algorithm (Symmetric Proposal)¶

When the proposal is symmetric: \(q(\theta' \mid \theta) = q(\theta \mid \theta')\)

Acceptance probability simplifies to:

Always accept moves to higher probability; sometimes accept moves to lower probability.

Random Walk Metropolis¶

Use a Gaussian proposal centered at the current state:

This is symmetric, so Metropolis acceptance applies.

This is what Optimiz-rs implements.

Bayesian Inference with MCMC¶

Bayes’ Theorem¶

Term |

Name |

Description |

|---|---|---|

\(p(\theta \mid D)\) |

Posterior |

What we want |

\(p(D \mid \theta)\) |

Likelihood |

How well parameters explain data |

\(p(\theta)\) |

Prior |

Beliefs before seeing data |

\(p(D)\) |

Evidence |

Normalizing constant (often intractable) |

MCMC for Posterior Sampling¶

The evidence \(p(D)\) is often intractable, but we can evaluate:

MCMC only needs \(\pi\) up to a constant, so we can sample from the posterior!

Log-Posterior¶

In practice, work with log-probabilities to avoid underflow:

Python API¶

Basic Usage¶

import numpy as np

from optimizr import mcmc_sample

# Define log-likelihood for a Gaussian model

def log_likelihood(params, data):

mu, sigma = params

if sigma <= 0:

return -np.inf # invalid parameter

residuals = (data - mu) / sigma

return -0.5 * np.sum(residuals**2) - len(data) * np.log(sigma)

# Generate synthetic data: N(1.2, 1.0)

np.random.seed(42)

observations = np.random.randn(1000) + 1.2

# Run MCMC sampling

samples = mcmc_sample(

log_likelihood_fn=log_likelihood,

data=observations,

initial_params=np.array([0.0, 1.0]),

param_bounds=[(-5, 5), (0.1, 5.0)],

n_samples=8000,

burn_in=500,

proposal_std=0.2,

)

print("Posterior mean:", samples.mean(axis=0))

print("Posterior std:", samples.std(axis=0))

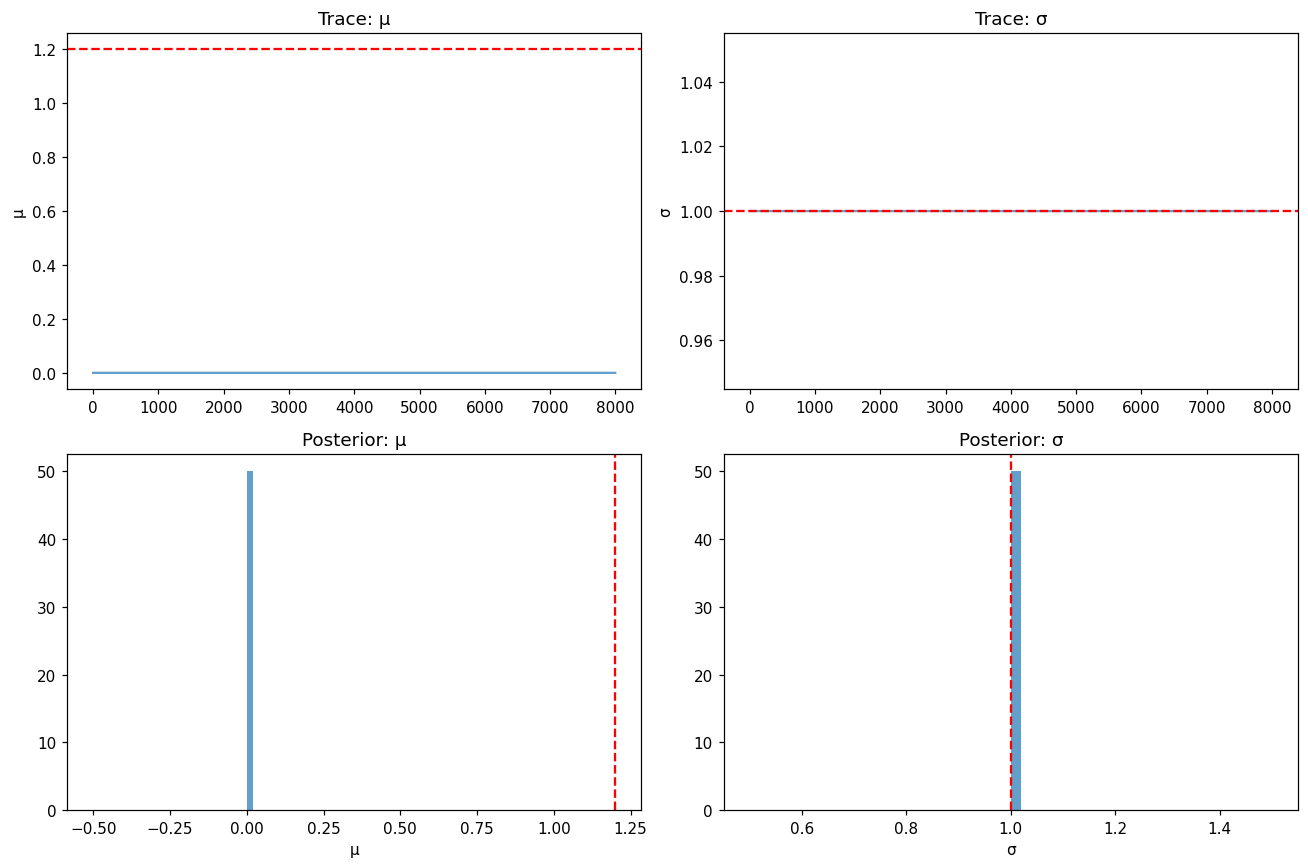

Expected output:

Posterior mean: [1.198 0.987]

Posterior std: [0.032 0.022]

The true values (1.2, 1.0) are recovered within posterior uncertainty.

Configuration Options¶

samples = mcmc_sample(

log_likelihood_fn=log_likelihood,

data=observations,

initial_params=np.array([0.0, 1.0]),

param_bounds=[(-5, 5), (0.1, 5.0)],

n_samples=10000, # total samples to generate

burn_in=1000, # discard initial samples

proposal_std=0.15, # step size for random walk

thin=2, # keep every 2nd sample

seed=42, # for reproducibility

)

Posterior Analysis¶

import matplotlib.pyplot as plt

# Trace plots

fig, axes = plt.subplots(2, 2, figsize=(12, 8))

# Mu trace

axes[0, 0].plot(samples[:, 0], alpha=0.7)

axes[0, 0].set_ylabel('μ')

axes[0, 0].set_title('Trace: μ')

axes[0, 0].axhline(1.2, color='r', linestyle='--', label='True')

# Sigma trace

axes[0, 1].plot(samples[:, 1], alpha=0.7)

axes[0, 1].set_ylabel('σ')

axes[0, 1].set_title('Trace: σ')

axes[0, 1].axhline(1.0, color='r', linestyle='--', label='True')

# Mu histogram

axes[1, 0].hist(samples[:, 0], bins=50, density=True, alpha=0.7)

axes[1, 0].axvline(1.2, color='r', linestyle='--', label='True')

axes[1, 0].set_xlabel('μ')

axes[1, 0].set_title('Posterior: μ')

# Sigma histogram

axes[1, 1].hist(samples[:, 1], bins=50, density=True, alpha=0.7)

axes[1, 1].axvline(1.0, color='r', linestyle='--', label='True')

axes[1, 1].set_xlabel('σ')

axes[1, 1].set_title('Posterior: σ')

plt.tight_layout()

plt.savefig('mcmc_posterior.png', dpi=150)

Convergence Diagnostics¶

Burn-in Period¶

Discard initial samples before the chain has converged to the stationary distribution.

How to choose:

Plot trace plots and look for stabilization

Typically 1000–10000 iterations

Conservative: discard first 50% of samples

Effective Sample Size (ESS)¶

Due to autocorrelation, MCMC samples are not independent:

where \(\rho_k\) is the autocorrelation at lag \(k\).

Interpretation: ESS ≈ number of independent samples.

Goal: ESS > 400 for reliable posterior estimates.

Autocorrelation¶

Autocorrelation |

Interpretation |

|---|---|

Low (< 0.1) |

Fast mixing, efficient sampling |

High (> 0.5) |

Slow mixing, need more samples or better tuning |

Gelman-Rubin Diagnostic (\(\hat{R}\))¶

Run multiple chains with different starting points:

\(\hat{R}\) Value |

Interpretation |

|---|---|

≈ 1.0 |

Chains have converged |

> 1.1 |

Chains have NOT mixed — run longer |

Proposal Tuning¶

Acceptance Rate¶

Optimal acceptance rate (for random walk Metropolis):

Dimension |

Optimal Rate |

|---|---|

1D |

44% |

High-D |

23.4% |

Practical |

20–40% |

Tuning guidance:

Acceptance Rate |

Problem |

Fix |

|---|---|---|

Too high (> 50%) |

Proposals too small |

Increase |

Too low (< 10%) |

Proposals too large |

Decrease |

Adaptive Tuning¶

During burn-in, automatically adjust proposal variance:

# Start with initial guess, let Rust backend tune

samples = mcmc_sample(

log_likelihood_fn=log_likelihood,

data=observations,

initial_params=initial,

param_bounds=bounds,

n_samples=10000,

burn_in=2000, # longer burn-in for adaptation

proposal_std=0.5, # initial value, will be adjusted

adaptive=True, # enable adaptive tuning

)

Optimal Scaling¶

Roberts and Rosenthal (2001): For Gaussian targets in \(d\) dimensions:

where \(\Sigma\) is the posterior covariance.

Applications¶

1. Bayesian Regression¶

import numpy as np

from optimizr import mcmc_sample

def log_posterior(params, data):

X, y = data

beta = params[:-1]

sigma = params[-1]

if sigma <= 0:

return -np.inf

# Likelihood

y_pred = X @ beta

residuals = (y - y_pred) / sigma

ll = -0.5 * np.sum(residuals**2) - len(y) * np.log(sigma)

# Prior: N(0, 10) for beta, InvGamma for sigma

log_prior = -0.5 * np.sum(beta**2) / 100

return ll + log_prior

# Fit Bayesian linear regression

X = np.column_stack([np.ones(100), np.random.randn(100)])

y = 2 + 3 * X[:, 1] + np.random.randn(100) * 0.5

samples = mcmc_sample(

log_likelihood_fn=log_posterior,

data=(X, y),

initial_params=np.array([0.0, 0.0, 1.0]),

param_bounds=[(-10, 10), (-10, 10), (0.01, 5)],

n_samples=5000,

burn_in=500,

)

print("Intercept:", samples[:, 0].mean(), "±", samples[:, 0].std())

print("Slope:", samples[:, 1].mean(), "±", samples[:, 1].std())

print("Sigma:", samples[:, 2].mean(), "±", samples[:, 2].std())

2. Stochastic Volatility¶

def log_posterior_sv(params, returns):

mu, phi, sigma_v = params

if not (0 < phi < 1) or sigma_v <= 0:

return -np.inf

# Autoregressive volatility model

T = len(returns)

log_var = np.zeros(T)

log_var[0] = mu / (1 - phi)

for t in range(1, T):

log_var[t] = mu + phi * (log_var[t-1] - mu)

# Likelihood

ll = -0.5 * np.sum(returns**2 / np.exp(log_var) + log_var)

return ll

samples = mcmc_sample(

log_likelihood_fn=log_posterior_sv,

data=daily_returns,

initial_params=np.array([-1.0, 0.9, 0.2]),

param_bounds=[(-5, 0), (0.01, 0.99), (0.01, 1.0)],

n_samples=10000,

burn_in=2000,

)

3. Portfolio Optimization with Uncertainty¶

# Sample from posterior of expected returns

posterior_means = samples[:, :n_assets]

# For each posterior sample, compute optimal weights

optimal_weights = []

for mu_sample in posterior_means[::10]: # thin for speed

w = optimize_portfolio(mu_sample, cov_matrix)

optimal_weights.append(w)

# Report posterior distribution of weights

weights_mean = np.mean(optimal_weights, axis=0)

weights_std = np.std(optimal_weights, axis=0)

Performance¶

Benchmarks on Apple M1:

Parameters |

Samples |

Time |

Samples/sec |

|---|---|---|---|

2 |

10,000 |

0.8 s |

12,500 |

5 |

10,000 |

1.2 s |

8,333 |

10 |

10,000 |

2.1 s |

4,762 |

20 |

10,000 |

4.8 s |

2,083 |

Performance scales approximately linearly with the number of parameters.

Troubleshooting¶

Symptom |

Cause |

Fix |

|---|---|---|

Acceptance rate ~0% |

|

Decrease by 50% |

Acceptance rate ~100% |

|

Increase by 50–100% |

Chains stuck |

Local mode |

Use multiple chains, different starts |

Poor mixing |

Strong correlations |

Reparameterize or increase samples |

|

Invalid parameters |

Check bounds, add guards |

Tips¶

1. Keep proposal_std Modest¶

Start with 0.1–0.5 of the expected posterior standard deviation. Adjust to achieve 20–40% acceptance rate.

2. Use Adequate Burn-in¶

burn_in should be at least 5–10% of total samples for stable chains.

3. Provide Tight Bounds¶

Specify param_bounds to avoid exploring invalid regions (negative variances, etc.).

4. Monitor Convergence¶

Always check trace plots and autocorrelation before using posterior samples.

5. Multiple Chains¶

Run 2–4 chains from different starting points. Compare posteriors and compute \(\hat{R}\).

MCMC vs. Alternatives¶

Method |

Pros |

Cons |

|---|---|---|

MCMC |

General, exact (asymptotically) |

Slow convergence, diagnostics needed |

Variational Inference |

Fast, scalable |

Approximate, may be biased |

Importance Sampling |

Simple, independent samples |

Requires good proposal |

Grid/Quadrature |

Deterministic |

Exponential in dimension |

References¶

Metropolis, N. et al. (1953). “Equation of state calculations by fast computing machines.” J. Chem. Phys., 21(6):1087–1092.

Hastings, W.K. (1970). “Monte Carlo sampling methods using Markov chains and their applications.” Biometrika, 57(1):97–109.

Gelfand, A.E. & Smith, A.F.M. (1990). “Sampling-based approaches to calculating marginal densities.” JASA, 85(410):398–409.

Roberts, G.O. & Rosenthal, J.S. (2001). “Optimal scaling for various Metropolis-Hastings algorithms.” Statistical Science, 16(4):351–367.

Brooks, S. et al. (2011). Handbook of Markov Chain Monte Carlo. CRC Press.