Optimal Control¶

This module provides advanced optimal control algorithms for financial applications, including Hamilton-Jacobi-Bellman (HJB) equation solvers, regime-switching models, parameter estimation, and state-space filtering. All algorithms are implemented in high-performance Rust with Python bindings.

Mathematical Foundations¶

Hamilton-Jacobi-Bellman (HJB) Equation¶

The HJB equation is a fundamental result in optimal control theory that provides the necessary and sufficient conditions for optimality of a control policy. For a stochastic control problem:

where \(V(x)\) is the value function, \(\rho\) is the discount rate, \(L\) is the running cost, and \(X_t\) follows a controlled stochastic process. The HJB equation is:

where \(\mathcal{L}^\alpha\) is the infinitesimal generator of the controlled process.

Application to Mean-Reverting Spreads¶

For pairs trading with an Ornstein-Uhlenbeck (OU) spread process:

with transaction costs \(c > 0\), the HJB equation becomes:

The optimal control is a threshold policy: buy when \(x < x_L\), sell when \(x > x_U\), hold otherwise.

Viscosity Solutions¶

Classical solutions to HJB equations rarely exist due to:

Non-smoothness at boundaries: The value function \(V(x)\) has kinks where the optimal control switches

Lack of regularity: Second derivatives \(V''(x)\) may not exist everywhere

Free boundary problems: The optimal switching thresholds \((x_L, x_U)\) are unknown

Viscosity solutions generalize the notion of solution to allow for non-smooth value functions. A function \(V\) is a viscosity solution if:

Subsolution property: For any smooth test function \(\phi\) such that \(V - \phi\) has a local maximum at \(x_0\): $\(\rho V(x_0) \leq \mathcal{H}(x_0, V(x_0), D\phi(x_0), D^2\phi(x_0))\)$

Supersolution property: For any smooth test function \(\psi\) such that \(V - \psi\) has a local minimum at \(x_0\): $\(\rho V(x_0) \geq \mathcal{H}(x_0, V(x_0), D\psi(x_0), D^2\psi(x_0))\)$

where \(\mathcal{H}\) is the Hamiltonian.

Key properties:

Uniqueness: Under suitable conditions (coercivity, proper discount), the viscosity solution is unique

Stability: Viscosity solutions are stable under uniform convergence

Numerical convergence: Monotone finite difference schemes converge to the viscosity solution

Finite Difference Methods¶

We discretize the HJB equation on a spatial grid \(x_i = x_{\min} + ih\), \(i = 0, \ldots, N\), with grid spacing \(h\).

Upwind Schemes¶

For the OU drift term \(\kappa(\theta - x)V'(x)\), we use upwind finite differences to ensure monotonicity and stability:

If \(\kappa(\theta - x_i) > 0\) (rightward drift): use forward difference $\(V'(x_i) \approx \frac{V_{i+1} - V_i}{h}\)$

If \(\kappa(\theta - x_i) < 0\) (leftward drift): use backward difference $\(V'(x_i) \approx \frac{V_i - V_{i-1}}{h}\)$

The diffusion term uses centered differences: $\(V''(x_i) \approx \frac{V_{i+1} - 2V_i + V_{i-1}}{h^2}\)$

Policy Iteration Algorithm¶

The HJB equation with control is solved via policy iteration:

Initialize: Start with policy \(\alpha^{(0)}\) (e.g., always hold)

Policy evaluation: Solve the linear system for value function \(V^{(k)}\): $\(\rho V^{(k)}_i = \mathcal{L}^{\alpha^{(k)}} V^{(k)}_i + L(x_i, \alpha^{(k)}_i)\)$

Policy improvement: Update policy by maximizing Hamiltonian: $\(\alpha^{(k+1)}_i = \arg\max_{\alpha} \{ \mathcal{L}^\alpha V^{(k)}_i + L(x_i, \alpha) \}\)$

Convergence check: If \(\|\alpha^{(k+1)} - \alpha^{(k)}\|_\infty < \epsilon\), stop; otherwise return to step 2

Convergence properties:

Typically 10-50 iterations for practical problems

Geometric convergence rate

Numerical solution converges to viscosity solution as \(h \to 0\)

Implemented Algorithms¶

1. HJB Solver for OU Process¶

Solves the optimal switching problem for mean-reverting spreads with transaction costs.

Implementation: src/optimal_control/hjb_solver.rs

Python API:

from optimizr import solve_hjb_py, solve_hjb_full_py

# Basic solver - returns optimal thresholds

lower, upper, residual, iters = solve_hjb_py(

kappa=3.0, # Mean reversion speed

theta=0.0, # Long-run mean

sigma=0.2, # Volatility

rho=0.04, # Discount rate

transaction_cost=0.001, # Transaction cost per trade

n_points=400, # Number of grid points

max_iter=4000, # Maximum policy iterations

tolerance=1e-7, # Convergence tolerance

n_std=5.0, # Grid extent in standard deviations

)

print(f"Optimal bounds: ({lower:.3f}, {upper:.3f})")

print(f"Residual: {residual:.2e}, Iterations: {iters}")

# Full solver - also returns value function and derivatives

lower, upper, residual, iters, V, V_x, V_xx = solve_hjb_full_py(

kappa=3.0, theta=0.0, sigma=0.2, rho=0.04,

transaction_cost=0.001, n_points=400

)

# Plot value function derivatives for diagnostics

import matplotlib.pyplot as plt

plt.plot(V_x)

plt.axvline(lower, color='r', linestyle='--', label='Lower bound')

plt.axvline(upper, color='g', linestyle='--', label='Upper bound')

plt.legend()

plt.title("Value function derivative V'(x)")

Parameters:

kappa: Mean reversion speed (typical range: 0.1-10). Higher values → faster reversion → narrower bandstheta: Long-run mean (typically 0 for normalized spreads)sigma: Volatility (typical range: 0.1-1.0). Higher values → wider bandsrho: Discount rate (typical: 0.01-0.1). Higher values → more myopic strategytransaction_cost: Per-trade cost (typical: 0.0001-0.01). Higher values → wider bands, fewer tradesn_points: Grid resolution (recommended: 200-500). Higher → more accurate but slowern_std: Grid extent (recommended: 3-6). Should cover 99%+ of spread distribution

Returns:

lower: Optimal buy threshold (negative value)upper: Optimal sell threshold (positive value)residual: Maximum policy change in last iteration (should be < tolerance)iters: Number of policy iterations (typically 10-50)V,V_x,V_xx: (full solver only) Value function and derivatives on grid

When to use:

Pairs trading with mean-reverting spreads

Statistical arbitrage with transaction costs

Optimal entry/exit for mean-reverting assets

Requires reliable OU parameter estimates (see OU estimation below)

Diagnostics:

Plot \(V'(x)\) to check smoothness near thresholds

Verify

residual < tolerancefor convergenceCheck that thresholds are within grid bounds

If not converged: increase

max_iteror adjust grid parameters

2. Viscosity Solution Solver¶

General-purpose viscosity solution solver for HJB equations with arbitrary Hamiltonians.

Implementation: src/optimal_control/viscosity.rs

Usage: Advanced users can extend this for custom control problems beyond OU switching.

3. Regime Switching Models¶

Optimal control with multiple market regimes, each with different dynamics.

Implementation: src/optimal_control/regime_switching.rs

Approach:

Use HMM to identify hidden regimes (see HMM section)

Estimate OU parameters per regime

Solve HJB per regime to get regime-specific thresholds

Switch control policy based on decoded regime

Example workflow:

from optimizr import HMM, estimate_ou_params_py, solve_hjb_py

import numpy as np

# Step 1: Train HMM on spread returns

returns = np.diff(spread)

hmm = HMM(n_states=2)

hmm.fit(returns.reshape(-1, 1), n_iterations=100)

regimes = hmm.predict(returns.reshape(-1, 1))

# Step 2: Estimate OU parameters per regime

params = []

for regime_id in range(2):

mask = (regimes == regime_id)

spread_regime = spread[1:][mask] # Align with returns

kappa, theta, sigma, half_life = estimate_ou_params_py(

spread_regime, dt=1/252

)

params.append((kappa, theta, sigma))

print(f"Regime {regime_id}: κ={kappa:.2f}, θ={theta:.3f}, σ={sigma:.3f}")

# Step 3: Solve HJB per regime

thresholds = []

for kappa, theta, sigma in params:

lower, upper, _, _ = solve_hjb_py(

kappa=kappa, theta=theta, sigma=sigma,

rho=0.04, transaction_cost=0.001

)

thresholds.append((lower, upper))

print(f"Thresholds: ({lower:.3f}, {upper:.3f})")

# Step 4: Apply regime-specific control

current_regime = regimes[-1]

lower, upper = thresholds[current_regime]

if spread[-1] < lower:

action = "BUY"

elif spread[-1] > upper:

action = "SELL"

else:

action = "HOLD"

print(f"Current regime: {current_regime}, Action: {action}")

4. Jump Diffusion Models¶

Extension of OU process with Poisson jumps for modeling sudden price shocks.

Implementation: src/optimal_control/jump_diffusion.rs

Model: $\( dX_t = \kappa(\theta - X_t)dt + \sigma dW_t + J_t dN_t \)$

where \(N_t\) is a Poisson process with intensity \(\lambda\), and \(J_t \sim \mathcal{N}(\mu_J, \sigma_J^2)\) are jump sizes.

Use case: Markets with flash crashes, earnings announcements, or other discontinuous events.

5. Multi-Regime Switching Jump Diffusion (MRSJD)¶

Combines regime switching with jump diffusion for maximum flexibility.

Implementation: src/optimal_control/mrsjd.rs

Model: Each regime has its own OU parameters AND jump process parameters.

Use case: Complex markets with both regime changes and sudden shocks (e.g., crypto, emerging markets).

6. OU Parameter Estimation¶

Estimates Ornstein-Uhlenbeck process parameters from time series data.

Implementation: src/optimal_control/ou_estimator.rs

Python API:

from optimizr import estimate_ou_params_py

import numpy as np

import matplotlib.pyplot as plt

# Simulate OU process (for testing)

dt = 1/252 # Daily data

T = 1000

kappa_true, theta_true, sigma_true = 3.0, 0.0, 0.2

rng = np.random.default_rng(0)

spread = [0.0]

for _ in range(T-1):

dx = kappa_true * (theta_true - spread[-1]) * dt + \

sigma_true * np.sqrt(dt) * rng.standard_normal()

spread.append(spread[-1] + dx)

spread = np.array(spread)

# Estimate parameters

kappa, theta, sigma, half_life = estimate_ou_params_py(spread, dt=dt)

print(f"True: κ={kappa_true:.2f}, θ={theta_true:.3f}, σ={sigma_true:.3f}")

print(f"Estimated: κ={kappa:.2f}, θ={theta:.3f}, σ={sigma:.3f}")

print(f"Half-life: {half_life:.1f} periods ({half_life*252:.1f} days)")

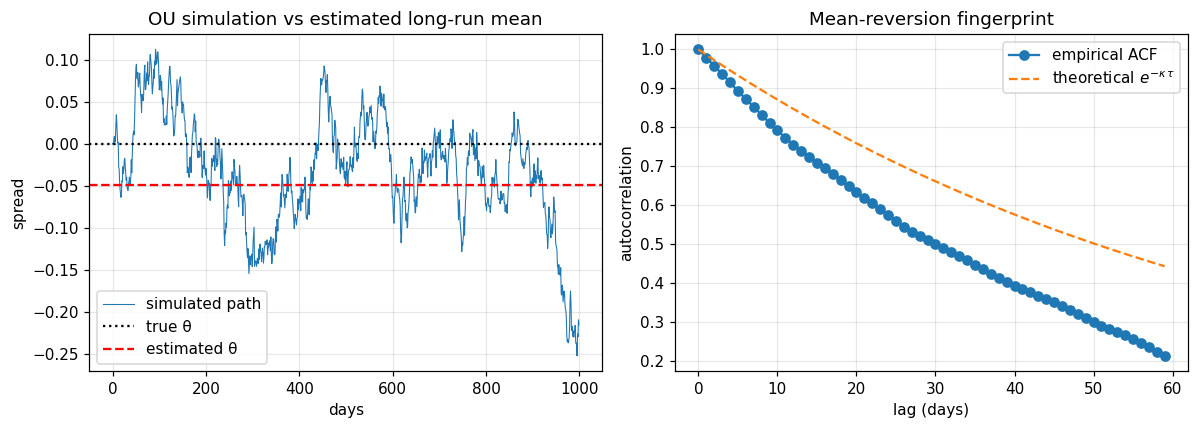

# Visualise the simulated path together with the estimated mean-reversion

# level and the decay envelope implied by the fitted half-life.

t_axis = np.arange(len(spread)) * dt * 252 # in days

fig, axes = plt.subplots(1, 2, figsize=(11, 4))

axes[0].plot(t_axis, spread, lw=0.7, label="simulated path")

axes[0].axhline(theta_true, color="k", ls=":", label="true θ")

axes[0].axhline(theta, color="red", ls="--", label="estimated θ")

axes[0].set_xlabel("days"); axes[0].set_ylabel("spread")

axes[0].set_title("OU simulation vs estimated long-run mean")

axes[0].legend(); axes[0].grid(alpha=0.3)

# Empirical autocorrelation vs theoretical exp(-κ τ).

lags = np.arange(0, 60)

x = spread - spread.mean()

acf = np.array([

(x[: len(x) - k] @ x[k:]) / (x @ x) for k in lags

])

axes[1].plot(lags, acf, "o-", label="empirical ACF")

axes[1].plot(lags, np.exp(-kappa * lags * dt), "--",

label=r"theoretical $e^{-\kappa\,\tau}$")

axes[1].set_xlabel("lag (days)"); axes[1].set_ylabel("autocorrelation")

axes[1].set_title("Mean-reversion fingerprint")

axes[1].legend(); axes[1].grid(alpha=0.3)

fig.tight_layout(); plt.show()

Method: Maximum likelihood estimation (MLE) using analytical formulas for discrete-time OU process.

Parameters:

spread: Time series of spread values (1D numpy array)dt: Time step in years (e.g., 1/252 for daily data, 1/52 for weekly)

Returns:

kappa: Mean reversion speed (annualized)theta: Long-run meansigma: Volatility (annualized)half_life: Half-life in time step units (\(\ln(2)/\kappa \cdot dt^{-1}\))

Practical tips:

Use at least 500-1000 observations for stable estimates

Check half-life: typical pairs have half-life 5-60 days

Winsorize extreme outliers (e.g., clip at ±5σ) if needed

For rolling estimates, use expanding or rolling windows of 250-500 periods

7. Kalman Filtering¶

State-space filtering for latent variable estimation and forecasting.

Implementation: src/optimal_control/kalman_filter.rs, src/optimal_control/kalman_py_bindings.rs

Linear Kalman Filter¶

For linear Gaussian state-space models: $\( \begin{aligned} x_{t+1} &= F x_t + B u_t + w_t, \quad w_t \sim \mathcal{N}(0, Q) \\ y_t &= H x_t + v_t, \quad v_t \sim \mathcal{N}(0, R) \end{aligned} \)$

Python API:

from optimizr import LinearKalmanFilter

import numpy as np

# Define system matrices

F = [[1.0, 1.0], [0.0, 1.0]] # State transition (2×2)

H = [[1.0, 0.0]] # Observation matrix (1×2)

Q = [[1e-4, 0.0], [0.0, 1e-4]] # Process noise covariance

R = [[1e-2]] # Measurement noise covariance

# Initialize filter

kf = LinearKalmanFilter(

f_matrix=F,

h_matrix=H,

q_matrix=Q,

r_matrix=R,

initial_state=[0.0, 0.0],

initial_covariance=[[1.0, 0.0], [0.0, 1.0]],

)

# Online filtering loop

observations = np.random.randn(100)

states = []

for obs in observations:

kf.predict(control=[0.0, 0.0]) # Prediction step

kf.update(observation=[obs]) # Correction step

state = kf.get_state()

states.append(state)

states = np.array(states)

print(f"Final state estimate: {states[-1]}")

Use cases:

Tracking latent spread dynamics with noise

State estimation for control (e.g., estimate velocity from noisy position)

Online parameter adaptation

Extended Kalman Filter (EKF)¶

For nonlinear systems with local linearization.

Use case: Nonlinear spread dynamics, regime probabilities as states.

Unscented Kalman Filter (UKF)¶

For highly nonlinear systems using sigma-point approximation.

Python API:

from optimizr import UnscentedKalmanFilter

ukf = UnscentedKalmanFilter(

state_dim=2,

obs_dim=1,

q_matrix=Q,

r_matrix=R,

initial_state=[0.0, 0.0],

initial_covariance=[[1.0, 0.0], [0.0, 1.0]],

)

# Similar predict/update interface

Use case: Jump diffusion models, volatility estimation, option pricing.

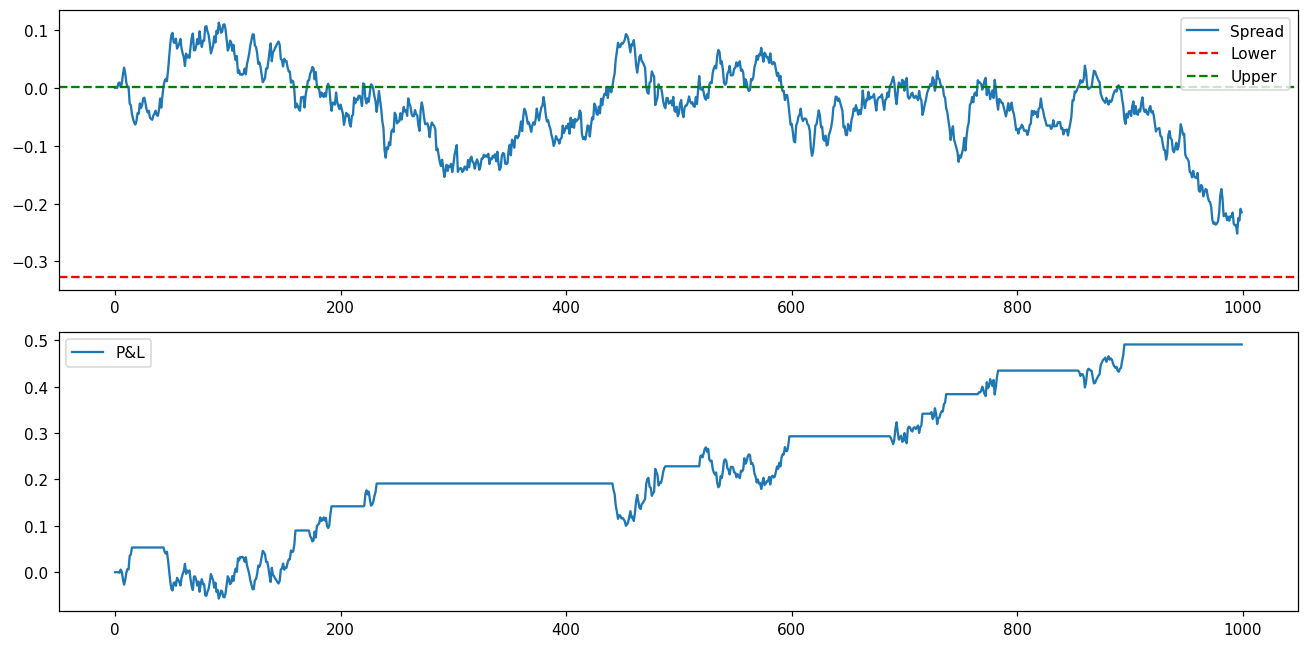

8. Backtesting Framework¶

Backtests optimal switching strategies on historical data.

Implementation: src/optimal_control/backtest.rs

Python API:

from optimizr import backtest_optimal_switching_py

# First, get optimal thresholds

lower, upper, _, _ = solve_hjb_py(

kappa=3.0, theta=0.0, sigma=0.2,

rho=0.04, transaction_cost=0.001

)

# Backtest on historical spread

metrics = backtest_optimal_switching_py(

spread=spread, # Historical spread data

lower_bound=lower, # Optimal buy threshold

upper_bound=upper, # Optimal sell threshold

transaction_cost=0.001, # Must match HJB solver

)

(

total_return, # Cumulative return

sharpe, # Annualized Sharpe ratio

max_dd, # Maximum drawdown

n_trades, # Number of round-trip trades

win_rate, # Fraction of profitable trades

pnl_path, # P&L time series

) = metrics

print(f"Return: {total_return:.2%}, Sharpe: {sharpe:.2f}")

print(f"Max DD: {max_dd:.2%}, Trades: {n_trades}, Win rate: {win_rate:.2%}")

# Plot P&L path

import matplotlib.pyplot as plt

plt.figure(figsize=(12, 6))

plt.subplot(2, 1, 1)

plt.plot(spread, label='Spread')

plt.axhline(lower, color='r', linestyle='--', label='Lower')

plt.axhline(upper, color='g', linestyle='--', label='Upper')

plt.legend()

plt.subplot(2, 1, 2)

plt.plot(pnl_path, label='P&L')

plt.legend()

plt.tight_layout()

Metrics interpretation:

total_return: Should be positive with low transaction costssharpe: Good values > 1.0, excellent > 2.0max_dd: Risk metric, compare to expected returnn_trades: Too many → excessive costs; too few → missing opportunitieswin_rate: Typically 40-60% for mean-reversion strategies

Parameter tuning:

If

win_ratelow butmax_ddhigh → bands too narrow, increasetransaction_costorrhoIf

n_tradeslow → bands too wide, decreasetransaction_costorrhoCompare Sharpe ratios across different parameter settings

Complete Workflow Example¶

Here’s a complete optimal control pipeline for pairs trading:

import numpy as np

import pandas as pd

from optimizr import (

estimate_ou_params_py,

solve_hjb_py,

backtest_optimal_switching_py,

HMM

)

# 1. Load price data (example with simulated data)

np.random.seed(42)

T = 5000

dt = 1/252

# Simulate cointegrated pair

price_A = 100 * np.exp(np.cumsum(0.0001 + 0.01*np.sqrt(dt)*np.random.randn(T)))

price_B = 100 * np.exp(np.cumsum(0.0001 + 0.01*np.sqrt(dt)*np.random.randn(T)))

spread = np.log(price_A) - np.log(price_B)

# Split into train/test

train_spread = spread[:3000]

test_spread = spread[3000:]

# 2. Estimate OU parameters

kappa, theta, sigma, half_life = estimate_ou_params_py(train_spread, dt=dt)

print(f"OU parameters: κ={kappa:.2f}, θ={theta:.3f}, σ={sigma:.3f}")

print(f"Half-life: {half_life:.1f} days")

# 3. Solve HJB for optimal thresholds

lower, upper, residual, iters = solve_hjb_py(

kappa=kappa,

theta=theta,

sigma=sigma,

rho=0.04,

transaction_cost=0.001,

n_points=400,

max_iter=2000,

tolerance=1e-7,

)

print(f"Optimal thresholds: ({lower:.3f}, {upper:.3f})")

print(f"Converged in {iters} iterations, residual={residual:.2e}")

# 4. Backtest on out-of-sample data

metrics = backtest_optimal_switching_py(

spread=test_spread,

lower_bound=lower,

upper_bound=upper,

transaction_cost=0.001,

)

total_return, sharpe, max_dd, n_trades, win_rate, pnl_path = metrics

print(f"\nBacktest Results:")

print(f" Total Return: {total_return:.2%}")

print(f" Sharpe Ratio: {sharpe:.2f}")

print(f" Max Drawdown: {max_dd:.2%}")

print(f" # Trades: {n_trades}")

print(f" Win Rate: {win_rate:.2%}")

# 5. Optional: Regime-aware control with HMM

returns = np.diff(train_spread)

hmm = HMM(n_states=2)

hmm.fit(returns.reshape(-1, 1), n_iterations=100)

regimes = hmm.predict(returns.reshape(-1, 1))

# Estimate OU per regime and get regime-specific thresholds

for regime_id in range(2):

mask = (regimes == regime_id)

spread_regime = train_spread[1:][mask]

k, t, s, _ = estimate_ou_params_py(spread_regime, dt=dt)

l, u, _, _ = solve_hjb_py(k, t, s, 0.04, 0.001)

print(f"Regime {regime_id}: κ={k:.2f}, thresholds=({l:.3f}, {u:.3f})")

Performance Characteristics¶

Computational Complexity¶

HJB Solver: \(O(N \cdot K)\) where \(N\) is

n_points, \(K\) is policy iterations (~10-50)OU Estimation: \(O(T)\) where \(T\) is time series length (closed-form MLE)

Kalman Filter: \(O(T \cdot d^3)\) where \(d\) is state dimension (matrix inversion per step)

Backtesting: \(O(T)\) single pass through data

Typical Runtimes (on modern CPU)¶

HJB solve (400 points): ~10-50ms

OU estimation (5000 samples): ~1ms

Kalman filter (1000 steps, 2D state): ~10ms

Backtest (5000 samples): ~5ms

Memory Requirements¶

HJB solver: \(O(N)\) for grid storage (~few KB)

Kalman filter: \(O(d^2)\) for covariance matrices (~few KB for small \(d\))

Backtesting: \(O(T)\) for P&L path storage (~few MB for long histories)

Integration with Other Modules¶

With Mean Field Games¶

Use optimal control as individual agent strategy

Aggregate across population for mean-field dynamics

See

algorithms/mean_field_games.mdfor MFG theory

With Sparse Optimization¶

Use Kalman-filtered states as inputs to sparse controllers

Combine L1-regularized control with HJB thresholds

See

algorithms/sparse_optimization.md

Troubleshooting¶

HJB solver not converging¶

Symptom:

residual > toleranceaftermax_iterFix: Increase

max_iter(try 5000-10000); reducetolerancerequirement; check that OU parameters are reasonable

Thresholds outside grid bounds¶

Symptom: Optimal thresholds at grid edges

Fix: Increase

n_std(try 6-8); check OU parameter estimates (very high σ needs wider grid)

OU estimates unstable¶

Symptom: Negative

kappaor extremehalf_lifeFix: Use more data (>1000 samples); check for non-stationarity; consider winsorizing outliers

Backtest Sharpe ratio low¶

Symptom: Sharpe < 0.5 despite positive thresholds

Fix: Check for regime changes (use HMM); verify spread is actually mean-reverting; adjust

transaction_costin HJB solver

Kalman filter diverging¶

Symptom: State estimates exploding

Fix: Check process noise

Qis not too large; verify observations are scaled properly; use UKF for strong nonlinearity

References¶

Optimal Control Theory¶

Fleming, W. H., & Soner, H. M. (2006). Controlled Markov Processes and Viscosity Solutions. Springer.

Øksendal, B. (2003). Stochastic Differential Equations: An Introduction with Applications (6th ed.). Springer.

Pham, H. (2009). Continuous-time Stochastic Control and Optimization with Financial Applications. Springer.

Viscosity Solutions¶

Barles, G., & Souganidis, P. E. (1991). Convergence of approximation schemes for fully nonlinear second order equations. Asymptotic Analysis, 4(3), 271-283.

Crandall, M. G., Ishii, H., & Lions, P.-L. (1992). User’s guide to viscosity solutions of second order partial differential equations. Bulletin of the American Mathematical Society, 27(1), 1-67.

Kalman Filtering¶

Kalman, R. E. (1960). A new approach to linear filtering and prediction problems. Journal of Basic Engineering, 82(1), 35-45.

Julier, S. J., & Uhlmann, J. K. (1997). New extension of the Kalman filter to nonlinear systems. Signal Processing, Sensor Fusion, and Target Recognition VI, 3068, 182-193.

Financial Applications¶

Avellaneda, M., & Lee, J.-H. (2010). Statistical arbitrage in the US equities market. Quantitative Finance, 10(7), 761-782.

Gatev, E., Goetzmann, W. N., & Rouwenhorst, K. G. (2006). Pairs trading: Performance of a relative-value arbitrage rule. The Review of Financial Studies, 19(3), 797-827.

See Also¶

HMM API Reference - Hidden Markov Models for regime detection

Mean Field Games - Population-level optimal control

Optimal Control API - Complete function signatures and types